Introduction

In this analysis, we delve into the current macroeconomic trends shaping the U.S. economy, focusing on the interplay between inflation, interest rates, and Federal Reserve policies. The U.S. economy is exhibiting a mix of resilience and emerging challenges, influenced by factors like consumer spending, labor market dynamics, supply chain stabilization, and broader fiscal conditions. We’ll examine the historical context of inflation, comparing past strategies and current policies of the Federal Reserve in their ongoing battle against rising prices. This investigation includes a detailed look at the latest economic indicators and predictions, specifically regarding the anticipated Federal Reserve’s interest rate decisions and their potential impacts on various aspects of the U.S. economy.

The world economy has indeed lost momentum from the impact of higher interest rates, the invasion of Ukraine, and widening geopolitical rifts, and it now faces new uncertainty from the war between Israel and Hamas militants, the International Monetary Fund warned recently.

A series of previous shocks, including the pandemic and Russia’s war in Ukraine, has slashed worldwide economic output by about $3.7 trillion over the past three years compared with pre-COVID trends.

It’s “too early” to assess the impact on global economic growth from the days-old war between Israel and the militant Palestinian group Hamas in Gaza, Gourinchas said.

Oil prices have risen by about 4% in the past several days and that has been seen in previous crises and previous conflicts and reflects the potential risk that there could be disruption either in production or transport of oil in the region. In the absence of declarations of support for Hamas from key oil producers Saudi Arabia, the United Arab Emirates, Kuwait, and Iraq, it would make it unlikely that they would restrict supply in response to the war, the impact has been muted. So far, the world economy has displayed remarkable resiliency.

The United States is a standout in the IMF’s latest World Economic Outlook, which was completed before the outbreak of war between Israel and Hamas. The IMF upgraded its forecast for U.S. growth this year to 2.1% (matching 2022) and 1.5% in 2024 (up sharply from the 1% it had predicted in July).

The U.S., an energy exporter, has not been hurt as much as countries in Europe and elsewhere by higher oil prices, which shot up after Russia invaded Ukraine last year and jumped more recently because of Saudi Arabia’s production cuts and American consumers have been more willing than most to spend the savings they accumulated during the pandemic.

Current macro-economic trend

The U.S. economy is navigating a cautiously optimistic path, with a blend of resilience and emerging challenges. Real GDP growth has been estimated at 2.0 to 2.4% in the first half of the year, hinting at the potential avoidance of recession. However, the Consumer Price Index (CPI) data brings a slightly cautious tone, having exceeded forecasts by hitting 0.4% Month-over-Month and 3.7% Year-over-Year, against expectations of 0.3% and 3.6% respectively. This increase from 3% in June to 3.7% in September suggests more persistent inflationary pressures than previously thought. The Core CPI, sitting at 4.1% after excluding volatile components, underlines this trend.

In response to the inflation dynamics, the Federal Reserve’s rate hikes, totaling 525 basis points since March 2022, may not conclude as anticipated. The Fed’s decision to hold rates constant currently might prelude tighter monetary policies in the future, especially as the labor market reports significant growth. Nonfarm payrolls in September saw the largest rise in eight months, with adjustments in prior months pointing to a stronger labor market. This robustness could prompt the Federal Reserve to consider further interest rate hikes.

Consumer spending continues to be a strong GDP driver, although it’s expected to moderate, potentially slowing growth to 0.5% by early 2024. The labor market’s current resilience, with a low unemployment rate, might face gradual cooling. Still, unemployment is anticipated to rise only slightly by 2024.

Supply chain issues have largely been resolved, and the housing market is stabilizing, albeit at low activity levels. However, rising inflation, tighter monetary policy, and challenges in commercial real estate, coupled with the recent U.S. credit rating downgrade by Fitch, could pose headwinds to economic growth. Furthermore, slower loan growth from regional banks and mounting fiscal challenges due to capped government spending could further influence the economic trajectory.

Thus, while the U.S. economy displays notable resilience amid a complex backdrop of inflationary pressures, robust labor market conditions, and policy shifts, the outlook remains mixed with careful optimism but underscored by vigilant monitoring of inflation and monetary policy responses.

Inflation in a historical content

Inflation has been a persistent challenge in the U.S. economy, influencing policy decisions over the centuries. Historically, responses to inflation have followed a cyclical pattern, often echoing broader economic trends. Last month’s Federal Reserve decision to increase the federal funds rate by 0.25 percent to counter the highest inflation since 1981 (between 6 percent and 8 percent annually) can be contextualized within this historical lens. The modest increase is aimed at curbing the current inflation surge, though it remains low by historical standards, at 0.25 to 0.50 percent.

Reflecting on the past, the late 1970s and early 1980s under Federal Reserve Chairman Paul Volcker saw drastic measures against inflation, raising rates to 17 percent, inducing a significant recession but ultimately controlling prices. This paved the way for a four-decade period of generally declining inflation and interest rates, contributing to a robust bond and stock market. Today, Federal Reserve Chairman Jerome Powell’s strategy echoes a more cautious approach, reminiscent of historical trends, raising concerns about the longevity of this period of low rates and inflation that commenced in the early 1980s.

Historical interest rates in the U.S. have fluctuated extensively. For instance, in 1790, ten-year government bonds carried a 6 percent interest rate, indicative of the period’s norms. Throughout the 19th century, although rates generally declined, they spiked during the War of 1812 and the Civil War, demonstrating how external factors like wars can impact economic conditions. Rates saw a low around 4 percent in 1898, then increased again around World War I, averaging less than 3 percent by 1946, before peaking at 15 percent in 1981.

These patterns show that inflation and interest rates have long been intertwined with socio-economic and political events, from Hamilton’s time to today’s pandemic-influenced economy. They underscore the complexity of managing inflation and its far-reaching implications, which continue to challenge policymakers. The current situation with modest rate hikes against a backdrop of significant monetary expansion and government spending raises questions about whether new strategies are required or if historical patterns will persist.

Fed’s Policies to Curb Inflation

The Federal Reserve, as the central bank of the United States, possesses a range of potent tools to combat inflation, a critical aspect of its mandate to ensure price stability and foster economic conditions conducive to sustainable growth. Primarily, the Fed utilizes interest rate adjustments as its chief instrument. By increasing the federal funds rate, the rate at which banks lend to each other overnight, the Fed can effectively make borrowing more expensive. This increase in cost of capital generally cools economic activity, as consumers and businesses are likely to reduce spending and investment, thereby dampening inflationary pressures. Another key tool is the management of the money supply through open market operations, involving the buying and selling of government securities. Selling these securities can absorb excess liquidity from the financial system, further helping to alleviate inflation.

Quantitative tightening, a relatively newer approach, involves reducing the holdings of long-term securities on the Fed’s balance sheet, thereby increasing long-term interest rates and slowing economic expansion. Additionally, the Fed’s communication strategy, often termed as ‘forward guidance’, plays a pivotal role in shaping market expectations around inflation and interest rate trajectories, influencing economic behavior. While the effectiveness of these tools can be influenced by various external factors, their calibrated application is central to the Fed’s strategy in containing inflation and maintaining economic stability.

The Federal Reserve’s Historical Stance

Historically, the Federal Reserve has tackled inflation through a mix of monetary policies, predominantly by manipulating interest rates and controlling the money supply. In the 1970s and early 1980s, the U.S. experienced high inflation, partly due to oil price shocks and loose fiscal policies. Under Chairman Paul Volcker, the Fed famously responded with a drastic monetary tightening, significantly raising the federal funds rate to curb the runaway inflation. This approach, although successful in reducing inflation, led to a sharp economic recession and high unemployment, highlighting the trade-offs involved in monetary policy decisions.

Throughout the 1990s and early 2000s, under Chairmen Alan Greenspan and Ben Bernanke, the Fed targeted inflation more indirectly, using interest rate adjustments in response to various economic indicators, not just inflation figures. This era saw the implementation of a de facto inflation targeting, even before the Fed officially adopted this policy in 2012. The Federal Open Market Committee (FOMC) consistently adjusted the federal funds rate to maintain inflation around a target rate, generally considered to be around 2%, stabilizing prices while fostering economic growth.

The Great Recession of 2008 saw the Fed adopting unconventional tools like Quantitative Easing (QE) – purchasing large-scale assets to inject liquidity into the economy. Post-2008, the Fed’s approach to inflation became more accommodative, keeping interest rates at historically low levels for an extended period to support economic recovery. The Fed’s historical strategies against inflation reveal a balance between managing price levels and supporting overall economic health, often requiring difficult choices with significant economic implications.

Economic Indicators and Predictions

However, the Fed’s November Interest Rate Decision, it is still expected to leave the rates unchanged, according to several surveys of the economists (CBSnews; CNBC; Forbes). Part of this could be due to the recent rise in longer-term interest rates which ‘equals’ one rate hike (according to Daly). The other part could be that wage growth seems to be cooling (Forbes). Moreover, the CME FedWatch Tool, which predicts Fed rate changes based on 30-Day Funds future pricing data, suggests a 99.9% probability of the target rate remaining at 525-550 bps after the November decision, with the other 0.1% chance of the rate falling back to 500-525 bps.

Nevertheless, it is more likely, albeit still not very probable, that rate hikes take place in December 2023 and January 2024, with probabilities of 19.8% and 26.0%, according to the CME FedWatch tool.

Conclusion

The U.S. economy, standing at a critical juncture, shows a blend of strength and vulnerability. With the Federal Reserve facing the intricate task of curbing inflation without triggering a recession, the road ahead is fraught with challenges and uncertainties. While historical precedents provide insight, the uniqueness of the current situation – marked by post-pandemic recovery, supply chain readjustments, and shifts in consumer behavior – necessitates a nuanced approach to monetary policy. The analysis of key economic indicators like unemployment rates, inflation trends, and bond yields indicates a cautiously optimistic outlook, yet underscores the need for vigilance and adaptability in policy-making. As we move toward the end of 2023 and into 2024, it remains crucial to monitor these indicators and the Federal Reserve’s responses to ensure a balanced and sustainable economic trajectory.

Appendix

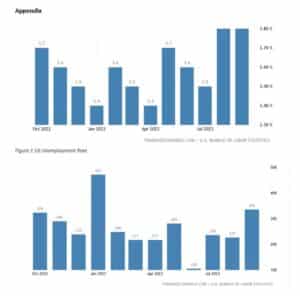

Figure 1 US Unemployment Rate

Figure 2 US Non-Farm Payroll

Figure 3 US Core CPI

Figure 4 US CPI

Figure 5 US Delinquency Rate

Figure 6 US 5 Year Treasury Bond Yield

Reference:

Bloomberg. (n.d.). United States rates & bonds. Bloomberg.com. https://www.bloomberg.com/markets/rates- bonds/government-bonds/us

Duggan, W. (2023, October 12). September inflation comes in higher than expected. Forbes. https://www.forbes.com/advisor/investing/current-inflation-rate/

Guardian News and Media. (2023, October 6). US economy added 336,000 jobs in September surpassing expectations. The Guardian. https://www.theguardian.com/business/2023/oct/06/jobs-report-september- economy-employment

Maureenegan. (2023, August 30). How liquid has the treasury market been in 2022?. Liberty Street Economics. https://libertystreeteconomics.newyorkfed.org/2022/11/how-liquid-has-the-treasury-market-been-in- 2022/

Published by Statista Research Department, & 12, S. (2023, September 12). Delinquency rate on consumer loans in the U.S. 2023. Statista. https://www.statista.com/statistics/1325074/delinquency-rate-on-consumer-loans-at-commercial-banks- in-the-us/#:~:text=In%20the%20second%20quarter%20of,been%20rising%20again%20since%202021.

United States consumer price index (cpi)september 2023 data – 1950-2022 historical. United States Consumer Price Index (CPI) – September 2023 Data – 1950-2022 Historical. (n.d.). https://tradingeconomics.com/united-states/consumer-price-index-cpi

United States unemployment rateseptember 2023 data – 1948-2022 historical. United States Unemployment Rate – September 2023 Data – 1948-2022 Historical. (n.d.). https://tradingeconomics.com/united- states/unemployment-rate

Leave A Comment