Spotlight – Energy George Rao

Introduction:

The energy sector has experienced a decline in deal volumes and average deal values in 2022; however, we anticipate that energy transition will remain a top priority for investors and management teams in 2023 and beyond. As a result, we expect significant capital allocation to mergers and acquisitions (M&A) and other capital project development activities within the energy, utilities, and resources (EU&R) sector. Furthermore, the focus on supply security, particularly for energy, renewables, and critical minerals, is becoming an increasingly important driver for M&A activity in both the EU&R sector and industrials businesses. Despite the challenges in obtaining traditional debt capital, the stronger balance sheets of EU&R businesses, coupled with the emergence of alternative debt providers, have allowed management teams to explore acquisitions. Notably, there has been a trend of businesses converging into different sectors or subsectors, such as chemical companies investing in renewables projects and oil and gas firms acquiring electricity retailers. This convergence is expected to continue and expand, attracting new investors and introducing added complexity to the EU&R M&A market, particularly in relation to supply chain resilience.

Industry Overview:

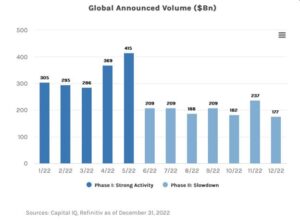

The energy sector is witnessing a surge in mergers and acquisitions (M&A) opportunities driven by the race to achieve carbon neutrality. In 2022, the global energy sector recorded a record-breaking year for M&A transactions, with 1,241 deals worth US$193.8 billion, making it the second-highest total since 2007. It is estimated that energy transition deals accounted for around 20% of all energy-sector M&A deals over US$1 billion in 2021. Europe, known for its progressive approach, has set ambitious renewable energy targets, although certain countries like Germany, the UK, and Italy are lagging behind. On the other hand, countries like Denmark, France, the Netherlands, Norway, and Sweden are better positioned and have a higher readiness for energy transition. The convergence of businesses into different sectors or subsectors, such as chemical companies entering the renewables market, is expected to accelerate, attracting new investors and adding complexity to the EU&R M&A market. In the United States, the Inflation Reduction Act has provided incentives for investment in renewable energy sources and related technologies, while a focus on carbon capture, utilization, and storage (CCUS) assets is gaining traction due to the abundance of cheap fossil fuels. In the Asia Pacific region, efforts to achieve a net-zero future are progressing, with significant renewables investment in China, India, and Australia. However, APAC still faces challenges in catching up to Europe and North America in terms of firm net-zero commitments. Overall, the energy sector’s journey toward achieving net-zero targets will continue to drive M&A activities in 2023 and beyond.

Industry Trend:

The energy sector is expected to experience an increase in mergers and acquisitions (M&A) activity in 2023, following a relatively quiet second half of 2022. Several factors are expected to drive this trend, including the deployment of capital by well-capitalized companies, the influence of activist investors, and the agreement between buyers and sellers on valuations and pricing.

One significant driver of M&A activity in the energy sector is the presence of well-capitalized companies looking to make acquisitions in their core businesses. Despite the consensus view of a mild recession in 2023, companies in the energy sector possess strong balance sheets, which can enable them to pursue strategic acquisitions even during an economic downturn. For example, energy companies with substantial capital resulting from soaring energy prices in 2022 may seek to deploy it through acquisitions or return it to shareholders. Additionally, mid-sized energy companies may pursue consolidation opportunities to enhance their competitiveness. Moreover, some energy companies are striving to improve their environmental, social, and governance (ESG) practices by acquiring capabilities such as carbon capture or energy transition preparedness.

Financial sponsors, such as private equity firms, also play a significant role in driving M&A activity in the energy sector. These firms currently hold record amounts of capital, known as dry powder, and are eager to deploy it in acquisitions. Private equity firms have become more specialized in specific industries and sub-sectors, allowing them to make investment decisions with confidence across different market cycles. Despite potential challenges in debt financing markets, the abundance of uninvested capital among private equity firms can contribute to increased M&A activity in the energy sector.

Another factor contributing to the trend is the prevalence of shareholder activism within the energy sector. The performance variance among companies due to the inflationary environment of the previous year has prompted activists to launch campaigns seeking changes that can create value. This trend is expected to continue in 2023, with activists demanding improvements in M&A strategies and operational performance. The relatively lower valuation levels in the market make it more feasible for activists to acquire stakes in public companies and launch campaigns with less downside valuation risk.

Cross-border M&A is anticipated to rebound in the energy sector after being dampened by the pandemic, trade tensions, and varying economic conditions in 2022. As the impact of these headwinds diminishes, companies worldwide are seeking to fortify their global supply chains, leading to increased international investments. While near-term focus may be on domestic markets, longer-term expectations suggest higher cross-border volumes between geographic regions.

Overall, industry experts at Morgan Stanley believe that the reduction in M&A activity experienced recently will be relatively short-lived compared to previous down cycles. The growth and specialization of the private equity industry, along with the strength of corporate balance sheets and earnings, are expected to support increased M&A activity in the energy sector in 2023 and beyond.

Six Key Factors that Influence the Energy Industry:

The energy industry is influenced by a variety of factors, including physical, human, and political aspects. These factors play a crucial role in determining energy supply and shaping the overall energy landscape. Here are the key factors that influence the energy industry:

- Geology and Access to Raw Materials: Geology is a significant physical factor that affects energy supply. The availability of fossil fuels like coal, crude oil, and natural gas is determined by the geological conditions in different regions. These resources formed millions of years ago under specific circumstances, resulting in their concentration in select areas of the world. Countries with favorable geological conditions have easier access to these resources, while others may need to rely on imports. The size, quality, and extraction complexity of these resources also impact their accessibility and cost-effectiveness.

- Climate and Renewable Energy Potential: Climate is another vital factor that influences the choice and feasibility of renewable energy sources. Different renewable energy technologies have specific climate requirements. For instance, hydroelectric power relies on consistent rainfall, while solar panels generate electricity from light rather than heat. Wind turbines require suitable wind conditions for optimal energy production. Thus, regional variations in climate determine the suitability and efficiency of different renewable energy sources.

- Environmental Conditions: Environmental conditions pose challenges in accessing certain energy resources. Extreme climates, such as very cold regions or high wave energy environments, can make resource extraction difficult and uneconomical. Examples include oil deposits in the oceans north of Alaska and potentially around Antarctica’s Great Southern Ocean. Extracting resources in such hazardous environments may require advanced technologies and substantial investment, which can influence the energy supply.

- Cost of Exploitation and Production: The cost of exploiting and producing energy resources significantly impacts energy prices. Factors such as labor costs, technological complexity, and accessibility play a role in determining production expenses. If wages or production costs increase, the overall cost of energy generation may rise as well. Economic considerations may lead to shifting production to regions with lower labor costs or more accessible resources. Changes in technology can also affect the cost-efficiency of energy production, either by enabling the extraction of previously uneconomic resources or by improving the efficiency of existing technologies.

- Technological Advancements: Technological advancements play a crucial role in the energy industry. New technologies can unlock previously inaccessible energy resources or enhance the efficiency of existing energy sources. For example, the development of fracking technology enabled the extraction of shale gas, while advancements in solar panel technology have increased their affordability and performance. Ongoing research, such as fusion power experiments, holds the potential to revolutionize energy generation in the future.

- Political Decisions and Policy Frameworks: Political factors significantly influence the energy industry through policy decisions and regulations. Government actions, such as setting renewable energy targets or imposing restrictions on certain energy sources, can shape the energy landscape. For instance, the UK government’s goal of banning the sale of diesel and petrol-powered cars by 2040 promotes the adoption of electric vehicles. International agreements, like the United Nations’ sustainable development goals, put pressure on governments to reduce fossil fuel use and prioritize renewable energy development.

In conclusion, the energy industry is influenced by a wide range of factors, including geological conditions, climate, environmental constraints, production costs, technological advancements, and political decisions. Understanding and addressing these factors are essential for shaping sustainable energy systems and ensuring reliable energy supply in the future.

Market Outlook:

The outlook for mergers and acquisitions (M&A) in the energy field, particularly in the oil and gas sector, is influenced by several factors outlined in the provided information. Despite economic and geopolitical pressures, M&A activity in the oil and gas industry has been on a downward trend, constituting only 3% of the industry’s market capitalization in recent years compared to a peak of 10% in 2014.

The shifting landscape of oil and gas M&A can be attributed to various factors. Firstly, the traditional correlation between M&A activity and oil prices has weakened. Instead, companies in the oil and gas sector are prioritizing capital discipline and directing free cash flows towards dividends and share buybacks. The focus on investing and acquiring for growth and increasing market share has been replaced by new drivers of M&A activity.

One significant trend in the energy field is the transition towards low-carbon and cleaner energy solutions. Oil and gas companies are pivoting their strategies to embrace low-carbon development and expansion into clean energy. Clean energy M&A reached a record high of $32 billion in 2022, constituting 15% of the total deal value by oil and gas firms. This shift reflects the industry’s efforts to adapt to changing market dynamics and investor expectations.

The five strategic moves that could reshape the dealmaking landscape in 2023 and beyond include:

- Debt-funded deals: Only 7% of oil and gas deals are funded by debt, indicating a reluctance to undertake debt and minimize the impact of potential interest rate hikes.

- Decoupling of oil price and M&A: The M&A playbook is changing, with M&A activity in the oil and gas sector becoming less dependent on oil prices.

- Focus on clean energy: Oil and gas companies are increasingly engaging in M&A activities related to clean energy assets, reflecting the industry’s commitment to the energy transition. This includes investments in solar, wind, biofuels, and hydrogen, among other clean energy sources.

- Energy security and trade: Energy security concerns and the desire to control supply chains have driven M&A activity in natural gas-based assets. Buyers are acquiring natural gas processing and takeaway capacity, particularly in regions like the Permian and Haynesville, to support increased exports.

- Improved governance and compliance: Oil and gas companies are forming joint ventures and strategic alliances in the clean energy space. This expansion covers a wider range of energy sources, fuels, and carbon-capture programs. Additionally, buyers are increasingly considering the environmental, social, and governance (ESG) profiles of sellers, with a preference for assets with higher ESG scores.

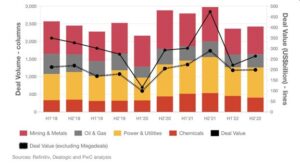

In terms of specific segments within the energy sector, upstream M&A activity has declined in value and count, reflecting shifting priorities towards rewarding shareholders and investing in clean energy. Midstream M&A, on the other hand, has seen an increase in deal count, driven by concerns around energy security and the growing role of natural gas. Oilfield services have experienced growth in deal count, particularly in exploration-specific assets and drilling rigs. Downstream M&A, however, has declined, with investor interest shifting towards customer-facing assets rather than traditional refinery assets.

To navigate the evolving energy landscape, companies are focusing on building resilience and creating a new core. This involves investment discipline, defensive M&A strategies, and the pursuit of clean energy opportunities. Embracing change and adapting to market dynamics are crucial for oil and gas companies seeking to thrive in the future.

Overall, the forecast for energy field M&A in 2023 and beyond suggests a continued shift towards clean energy, strategic partnerships, and a changing playbook that is less reliant on oil prices. The industry’s transformation towards a more sustainable and diversified energy portfolio is expected to shape the dealmaking landscape in the coming years.

Conclusion:

In conclusion, the energy sector is poised for increased mergers and acquisitions (M&A) activity in 2023 and beyond, driven by the focus on energy transition and the pursuit of net-zero targets. Despite a decline in M&A volumes and values in 2022, the industry is expected to rebound due to factors such as well-capitalized companies seeking acquisitions in their core businesses, the influence of activist investors demanding changes and improvements, and the availability of dry powder among financial sponsors. Cross-border M&A is also anticipated to rebound as companies aim to fortify their global supply chains. The industry is influenced by key factors including geology, climate, environmental conditions, production costs, technological advancements, and political decisions. Understanding and addressing these factors will be essential for shaping sustainable energy systems and ensuring a reliable energy supply in the future. The oil and gas sector, in particular, is experiencing a shift towards low-carbon and cleaner energy solutions, with companies embracing clean energy M&A and diversifying their portfolios. The market outlook suggests a changing playbook for M&A, with a focus on debt-funded deals, decoupling from oil prices, clean energy investments, energy security, and improved governance and compliance. By embracing change and adapting to market dynamics, energy companies can navigate the evolving landscape and thrive in the future.

References:

- https://mergers.whitecase.com/highlights/there-is-no-turning-back-for-the-global-energy-transition#:~:text=The%20global%20energy%20sector%20had,second%2Dhighest%20total%20since%202007.

- https://www.pwc.com/gx/en/services/deals/trends/energy-utilities-resources.html

- https://www.morganstanley.com/ideas/mergers-and-acquisitions-outlook-2023-trends

- https://www.coolgeography.co.uk/gcsen/CRM_Energy_Factors_Supply.php

- https://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-gas-mergers-and-acquisitions.html

Leave A Comment